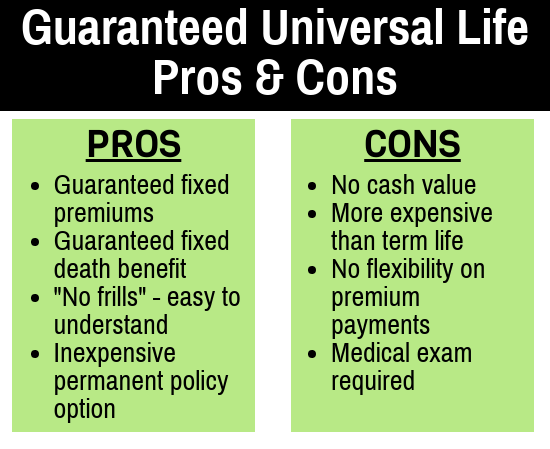

Universal life insurance can be a valuable investment for many individuals, offering flexibility and potential financial security. However, it’s essential to consider the pros and cons of any insurance policy. In this article, we will explore the disadvantages of universal life insurance so you can make an informed decision about your financial future.

While universal life insurance offers benefits such as cash value accumulation and the ability to adjust your premiums and death benefits, there are a few drawbacks to be aware of. One disadvantage is the potential for high fees and expenses associated with universal life policies. These costs can eat into your cash value and overall returns, reducing the long-term value of your policy. Additionally, universal life insurance may have complex and confusing policy terms, making it difficult to understand your coverage details fully. This lack of transparency can lead to surprises or misunderstandings down the line. It’s important to carefully review and understand the terms and conditions of any policy before committing to it.

Furthermore, universal life insurance is not suitable for everyone. If you have short-term insurance needs or are primarily focused on term life insurance coverage, a universal life policy may not be the best fit for you. Additionally, if you’re looking for a straightforward, low-maintenance insurance option, universal life insurance may not be the right choice. It requires ongoing monitoring and management to ensure the policy remains on track to meet your goals. By considering the disadvantages of universal life insurance alongside its benefits, you can make an informed decision about whether it aligns with your financial needs and priorities.

Understanding the Disadvantages of Universal Life Insurance

Universal life insurance is popular for individuals seeking a flexible, long-term coverage option. However, like any financial product, it has disadvantages. Understanding these drawbacks before making a decision is essential. This article will explore some of the critical disadvantages of universal life insurance and how they may impact your financial planning.

1. Premium Flexibility

One of the main advantages of universal life insurance is its flexibility in premium payments. However, this flexibility can also be a disadvantage. If you choose to pay lower premiums, there is a risk that the policy’s cash value may not grow enough to cover the insurance cost. This can reduce the death benefit or the policy’s lapse if the cash value is depleted. It is crucial to carefully consider your premium payment strategy to ensure the long-term sustainability of the policy.

Another aspect of premium flexibility is the potential for premium increases. Universal life insurance policies often have adjustable premium rates, meaning the insurer can raise premiums if certain conditions are met. This can be a significant disadvantage, especially for individuals with fixed incomes or limited financial resources. Therefore, reviewing your policy regularly and preparing for potential premium increases is essential.

2. Complexity and Cost

Universal life insurance is known for its complexity, which can disadvantage some individuals. Unlike term life insurance, which offers straightforward coverage for a specific period, universal life insurance combines a death benefit with a savings component. Understanding the policy’s intricacies, such as the cost of insurance charges, interest rates, and surrender fees, can be challenging.

Additionally, universal life insurance tends to be more expensive than term life insurance. This is because a portion of the premium goes towards the cash value accumulation, which is not valid with term insurance. The higher cost can make universal life insurance less accessible for individuals on a tight budget or those looking for a more affordable insurance option.

3. Investment Risk

Universal life insurance policies often offer various investment options for the cash value portion of the policy. While this can be advantageous for individuals seeking potential growth, it also exposes them to investment risk. The performance of the investments can directly impact the cash value and, consequently, the death benefit.

If the investments perform poorly, the cash value may not grow as expected, and the policy may not provide the desired coverage. This risk can be mitigated by carefully selecting investment options and regularly reviewing the performance of the policy. However, risk-averse individuals may prefer a more stable and predictable life insurance option.

4. Policy Surrender Charges

One must be aware of policy surrender charges when considering universal life insurance. These charges are applied if you cancel or surrender the policy before a certain period, typically within the first 10 to 15 years. The surrender charges can be substantial and significantly reduce the cash value you receive if you decide to terminate the policy.

It is crucial to carefully evaluate your long-term commitment to the policy before purchasing universal life insurance. Suppose there is a possibility that you may need to cancel the policy shortly. In that case, other life insurance options with lower or no surrender charges may be worth considering.

5. Potential Policy Lapse

Another disadvantage of universal life insurance is the risk of policy lapse. As mentioned earlier, if the cash value is insufficient to cover the insurance cost, the policy may lapse, resulting in a loss of coverage. This can happen if the policy owner does not monitor the policy’s performance or fails to adjust premium payments accordingly.

To avoid a policy lapse, it is essential to regularly review the policy’s cash value, premium payments, and any changes in your financial circumstances. This proactive approach will help ensure the policy remains active and provides the intended coverage.

In conclusion, while universal life insurance offers flexibility and long-term coverage, its disadvantages must also be considered. Premium flexibility, complexity and cost, investment risk, policy surrender charges, and potential policy lapse are all factors that should be carefully evaluated before making a decision. Consulting with a financial advisor can help you navigate the complexities of universal life insurance and determine if it is the right choice for your financial needs.

Key Takeaways: Disadvantages of Universal Life Insurance

- 1. Universal life insurance can be expensive compared to other types of life insurance.

- 2. The investment component of universal life insurance can be complex and risky.

- 3. If the policyholder doesn’t pay enough premiums, the policy could lapse, and coverage may be lost.

- 4. Universal life insurance policies may have surrender charges if the policyholder wants to cancel the policy early.

- 5. The cash value growth of universal life insurance policies may not perform as expected.

Frequently Asked Questions

Question 1: How does universal life insurance work?

Universal life insurance is permanent life insurance that offers a death benefit and a cash value component. It allows policyholders to accumulate savings tax-deferred while providing coverage for their entire lifetime. The premiums paid into the policy are divided into two parts: one goes towards the insurance cost, and the other is allocated to the cash value account.

While universal life insurance offers flexibility regarding premium payments and death benefit options, it also has some disadvantages that should be considered.

Question 2: What are the disadvantages of universal life insurance?

One of the main disadvantages of universal life insurance is its cost. Compared to term life insurance, the premiums for universal life insurance tend to be higher. This is because part of the premium goes towards the policy’s cash value, resulting in a higher overall cost.

Another disadvantage is the complexity of universal life insurance policies. The cash value component, investment options, and other features can confuse policyholders. Additionally, policyholders need to monitor the cash value account and ensure that it is sufficient to cover the cost of insurance and other expenses.

Question 3: Can the cash value of a universal life insurance policy decrease?

Yes, the cash value of a universal life insurance policy can decrease. The cash value is tied to the performance of the policyholder’s underlying investments. If the investments perform poorly, the cash value can fall, potentially impacting the policy’s ability to cover the cost of insurance.

It’s important to note that the cash value can also fluctuate based on changes in interest rates or fees associated with the policy. Policyholders should regularly review their policies to ensure the cash value meets their expectations.

Question 4: Are there surrender charges associated with universal life insurance?

Yes, surrender charges are a common feature of universal life insurance policies. These charges are imposed when a policyholder wants to surrender or cancel their policy before the end of the surrender period, typically a specified number of years after the policy is issued.

The surrender charges can be substantial, especially in the policy’s early years. Policyholders need to understand and consider them when evaluating the suitability of a universal life insurance policy.

Question 5: What happens if I stop paying premiums on my universal life insurance policy?

If you stop paying premiums on your universal life insurance policy, the cash value can be used to cover the insurance cost for a certain period. However, if the cash value is insufficient to cover the premiums, the policy may lapse, resulting in a loss of coverage.

Policyholders should be aware of the consequences of stopping premium payments and consider alternative options, such as reducing the death benefit or utilizing the policy’s cash value to keep the policy in force.

Final Summary: The Drawbacks of Universal Life Insurance

Considering the potential disadvantages and benefits of universal life insurance is essential. While this type of policy offers flexibility and a cash value component, it also has a few drawbacks.

One key disadvantage is the cost. Universal life insurance tends to be more expensive than other types, such as term life insurance. The premiums can be higher due to the added investment component and the potential for cash value accumulation, making it less affordable for those on a tight budget.

Another drawback is the complexity of universal life insurance. This type of policy can be more challenging to understand than straightforward options like term life insurance. Universal life insurance involves managing investment and monitoring cash value growth. It requires regular attention and potentially adjusting the premiums and death benefit. This complexity can be overwhelming for some individuals who prefer a more straightforward insurance solution.

In conclusion, while universal life insurance offers certain advantages, such as flexibility and the potential to build cash value, it has its fair share of disadvantages. The higher cost and complexity may not be suitable for everyone. Before deciding if universal life insurance suits you, it’s crucial to carefully weigh the pros and cons and consider your financial situation and long-term goals. Remember to consult a qualified insurance professional who can provide personalized advice based on your needs and circumstances.