If you’re a small business owner, you know how important it is to protect yourself from potential liabilities. One way to do that is by having liability insurance. But how much does liability insurance cost for a small business? This article will dive into small business liability insurance and explore the factors influencing its price. So, grab a cup of coffee and get ready to learn about this crucial aspect of running a business!

Liability insurance for a small business can vary in cost depending on several factors. The size and nature of your business, the industry you operate in, and the coverage limits you choose can all play a role in determining the price. Your location and claims history can also affect the cost of your policy. While there is no one-size-fits-all answer to how much liability insurance for small businesses costs, understanding these factors can help you better understand what to expect. So, let’s break it down and demystify the world of small business liability insurance!

How Much Is Liability Insurance for a Small Business?

Liability insurance is an essential investment for small businesses, providing financial protection in case of accidents, injuries, or property damage during business operations. However, determining the cost of liability insurance can be complex as it depends on several factors. In this article, we will explore the various aspects that affect the price of liability insurance for small businesses, helping you understand how much you can expect to pay and how to find the best coverage for your needs.

Factors Affecting the Cost of Liability Insurance

When determining the cost of liability insurance for a small business, several key factors come into play. These factors include:

Type of Business

The type of business you operate plays a significant role in determining the cost of liability insurance. Businesses considered high-risk, such as construction companies or medical practices, may face higher premiums due to the increased likelihood of accidents or damages. On the other hand, low-risk businesses, such as consulting firms or online retailers, may enjoy lower insurance premiums.

Business Size

The size of your small business can also impact the liability insurance cost. Generally, larger companies with more employees and higher revenue may have higher insurance costs than smaller ones. This is because larger businesses typically have more exposure to potential risks and may require higher coverage limits.

However, it’s important to note that insurance providers also consider your business’s specific operations and revenue when determining your premium, so the size of your business is just one piece of the puzzle.

Location

The location of your small business can influence the cost of liability insurance. Insurance providers consider factors such as local laws, regulations, and the overall risk profile of the area when determining premiums. For example, businesses in areas prone to natural disasters or with higher crime rates may face higher insurance costs.

Claims History

Your business’s claims history can impact the cost of liability insurance. If your company has a history of frequent or costly claims, insurance providers may view you as a higher risk and adjust your premiums accordingly. On the other hand, a clean claims history can potentially lower your insurance costs.

How to Find Affordable Liability Insurance

Now that we understand the factors that affect the cost of liability insurance for small businesses let’s explore some tips to help you find affordable coverage:

Shop Around

One of the most effective ways to find affordable liability insurance is to shop around and compare quotes from multiple insurance providers. Different insurance companies may offer varying rates and coverage options, so it’s essential to research and explore other options before deciding.

Bundle Policies

Some insurance providers offer discounts if you bundle multiple insurance policies together. Consider consolidating your business’s insurance needs, such as general liability, property insurance, and professional liability, with one insurer to save on premiums potentially.

Implement Risk Management Strategies

You can reduce your liability insurance costs by implementing risk management strategies and minimizing potential risks. This can include implementing safety protocols, providing employee training, and regularly maintaining equipment and premises.

Consider Deductibles and Coverage Limits

Adjusting your deductibles and coverage limits can help you find affordable liability insurance. A higher deductible means you will pay more out of pocket in the event of a claim, but it can lower your premium. Similarly, adjusting your coverage limits to align with your business’s needs can help avoid overpaying for unnecessary coverage.

The Importance of Liability Insurance for Small Businesses

Liability insurance is crucial for small businesses as it provides financial protection and peace of mind. Accidents and unexpected events can happen at any time, and without liability insurance, your company may be at risk of significant financial losses. With the right coverage, you can protect your business assets, cover legal expenses, and continue operating despite adversity.

In conclusion, the cost of liability insurance for a small business depends on various factors such as the type of business, business size, location, and claims history. It’s essential to shop around, compare quotes, and consider risk management strategies to find affordable coverage. Remember, liability insurance is a necessary investment to safeguard your business from potential risks and ensure its long-term success.

Key Takeaways: How Much is Liability Insurance for a Small Business?

- Liability insurance costs for small businesses can vary depending on industry, location, and coverage needs.

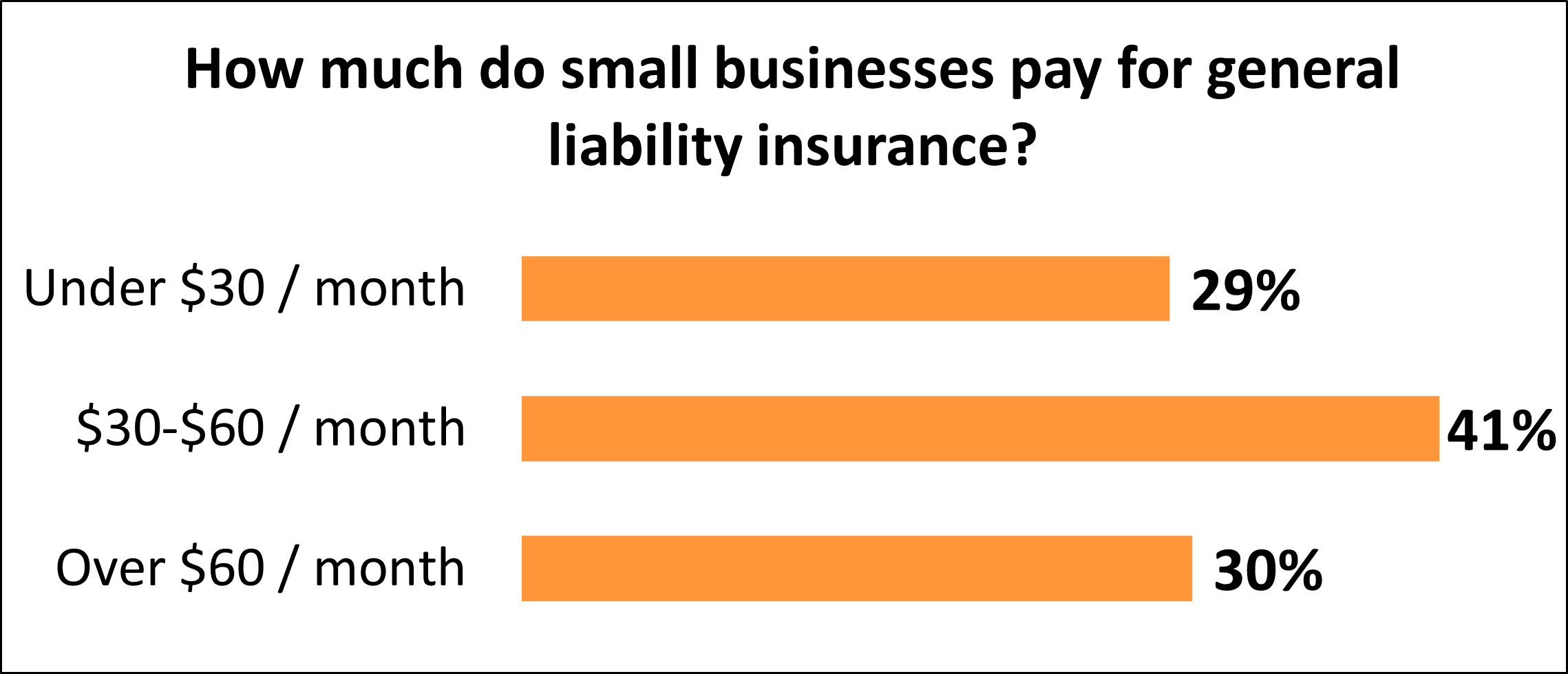

- On average, small businesses can expect to pay around $500 to $3,000 annually for liability insurance.

- Factors that can affect liability insurance costs include the business size, annual revenue, and the type of coverage chosen.

- Before purchasing liability insurance, small business owners need to assess their specific risks and coverage needs.

- Comparing quotes from multiple insurance providers can help small business owners find the best coverage at the most affordable price.

Frequently Asked Questions

What factors determine the cost of liability insurance for a small business?

Several factors can influence the cost of liability insurance for a small business. First and foremost, your business type plays a significant role. High-risk industries, such as construction or healthcare, typically have higher premiums due to the increased likelihood of accidents or claims. The size of your business and its annual revenue are also important factors. Larger companies may require higher coverage limits, resulting in higher premiums. Additionally, the location of your business can impact the cost of liability insurance, as certain areas may have higher claim rates or legal requirements.

Other factors affecting the cost include the number of employees, the coverage limits you choose, and any past claims history. Insurance companies also consider the level of risk associated with your specific business operations and the likelihood of potential claims. For an accurate quote, consulting with insurance providers specializing in small business liability coverage is best.

What is the average cost of liability insurance for a small business?

The average cost of liability insurance for a small business can vary depending on various factors. On average, small companies may expect to pay anywhere from $400 to $1,500 per year for general liability coverage. This estimate is based on businesses with low-risk operations and minimal coverage needs. However, it’s essential to remember that each business is unique, and the actual cost may differ based on industry, location, and other factors.

Obtaining quotes from multiple insurance providers to compare prices and coverage options is recommended. This allows you to find the best liability insurance policy that suits your business needs and budget. Additionally, consider working with an insurance agent or broker specializing in small business insurance, as they can provide valuable guidance and help you navigate the options.

Are there any additional types of liability insurance that small businesses should consider?

While general liability insurance is essential for most small businesses, additional liability coverage may be beneficial depending on your industry and specific needs. One common type is professional liability insurance, also known as errors and omissions insurance. This coverage protects businesses from claims of negligence, errors, or inadequate work in professional services.

Other types of liability insurance to consider include product liability insurance, which covers claims related to products sold or manufactured by your business, and cyber liability insurance, which protects against data breaches and cyberattacks. Assessing your business activities and potential risks is crucial to determine if additional liability coverage is necessary.

Can I save money on liability insurance for my small business?

You can employ several strategies to save money on liability insurance for your small business. First, consider bundling your policies with the same insurance provider. Many insurers offer discounts for combining multiple types of coverage, such as general liability and property insurance.

Additionally, implementing risk management practices and maintaining a safe working environment can help reduce your premiums. Insurance providers often reward businesses that have implemented safety measures and have a low claims history. You can also consider increasing your deductible, which can lower your premiums, but remember that you’ll be responsible for a higher out-of-pocket expense in case of a claim.

Do I legally need liability insurance for my small business?

The legal requirement for liability insurance varies depending on the jurisdiction and the type of business you operate. Some states or industries may have specific regulations that mandate certain types of coverage. For example, professional services businesses may require professional liability insurance. Researching and understanding the insurance requirements specific to your location and industry is essential.

Protecting your business from potential risks and financial losses is highly recommended, even if liability insurance is not legally required. A single claim or lawsuit can significantly impact your business’s finances, reputation, and stability. Liability insurance provides a safety net and peace of mind, allowing you to focus on running and growing your business without unnecessary worries.

How Much Does Small Business Insurance Cost?

Final Thoughts on How Much Liability Insurance Costs for a Small Business

After delving into the world of liability insurance for small businesses, it’s clear that the cost can vary significantly. At the same time, there is no one-size-fits-all answer to how much liability insurance costs; small business owners need to understand the factors that influence pricing. Several variables are at play, from the type of business to the coverage limits and industry-specific risks.

When determining the cost of liability insurance, it’s crucial to consider your business’s potential risks. Discussing your specific needs with an insurance provider can ensure you have the right coverage to protect your business and peace of mind. While cost isessentialt, it shouldn’t be the sole factor in your decision-making process. It’s worth investing in comprehensive liability insurance to safeguard your business from unexpected events that could otherwise lead to financial strain.

In conclusion, small business liability insurance costs vary depending on numerous factors. By thoroughly assessing your business’s needs and consulting with insurance professionals, you can find a policy that provides adequate coverage at a price that aligns with your budget. So, don’t delay protecting your business; take the necessary steps to secure the right liability insurance today. It’s an investment that can save you from potential financial setbacks in the future.