If you’re a business owner, you’ve probably asked yourself, “Does my business insurance cover independent contractors?” It’s a valid question that deserves a clear and concise answer. After all, understanding the scope of your insurance coverage is crucial for protecting your business and its assets. In this article, we’ll dive into business insurance and explore whether or not it extends to independent contractors.

When running a business, it’s essential to have a safety net in place. That’s where business insurance comes in. It covers various risks, including property damage, liability claims, and employee injuries. But what about independent contractors? These individuals often work for your business on a project-by-project basis, but does your insurance policy cover them? The answer is not always straightforward, so let’s unravel the complexities and shed some light on this critical topic. So, please grab a cup of coffee and get down to business!

Your business insurance may cover independent contractors, depending on your policy. Some business insurance policies may automatically cover independent contractors, while others may require you to add them as additional insured. Reviewing your policy and consulting with your insurance provider to understand the specific coverage for independent contractors is essential.

Does My Business Insurance Cover Independent Contractors?

As a business owner, you may wonder if your insurance coverage extends to independent contractors. It’s an important question, as the answer can significantly affect your business and its financial security. This article will explore whether business insurance covers independent contractors, providing valuable information and insights to help you make informed decisions.

Understanding Independent Contractors and Business Insurance

Independent contractors work for themselves and provide services to other businesses. They are not employees and, as such, are not typically covered by the same insurance policies that protect your employees. While your business insurance may provide employee coverage, reviewing your policy to determine if it includes or excludes independent contractors is essential.

There are a few key factors to consider regarding insurance coverage for independent contractors. These include the type of insurance policy you have, the nature of the work performed by the independent contractor, and the specific terms and conditions outlined in your policy. Let’s explore these factors in more detail.

Types of Insurance Policies That May Cover Independent Contractors

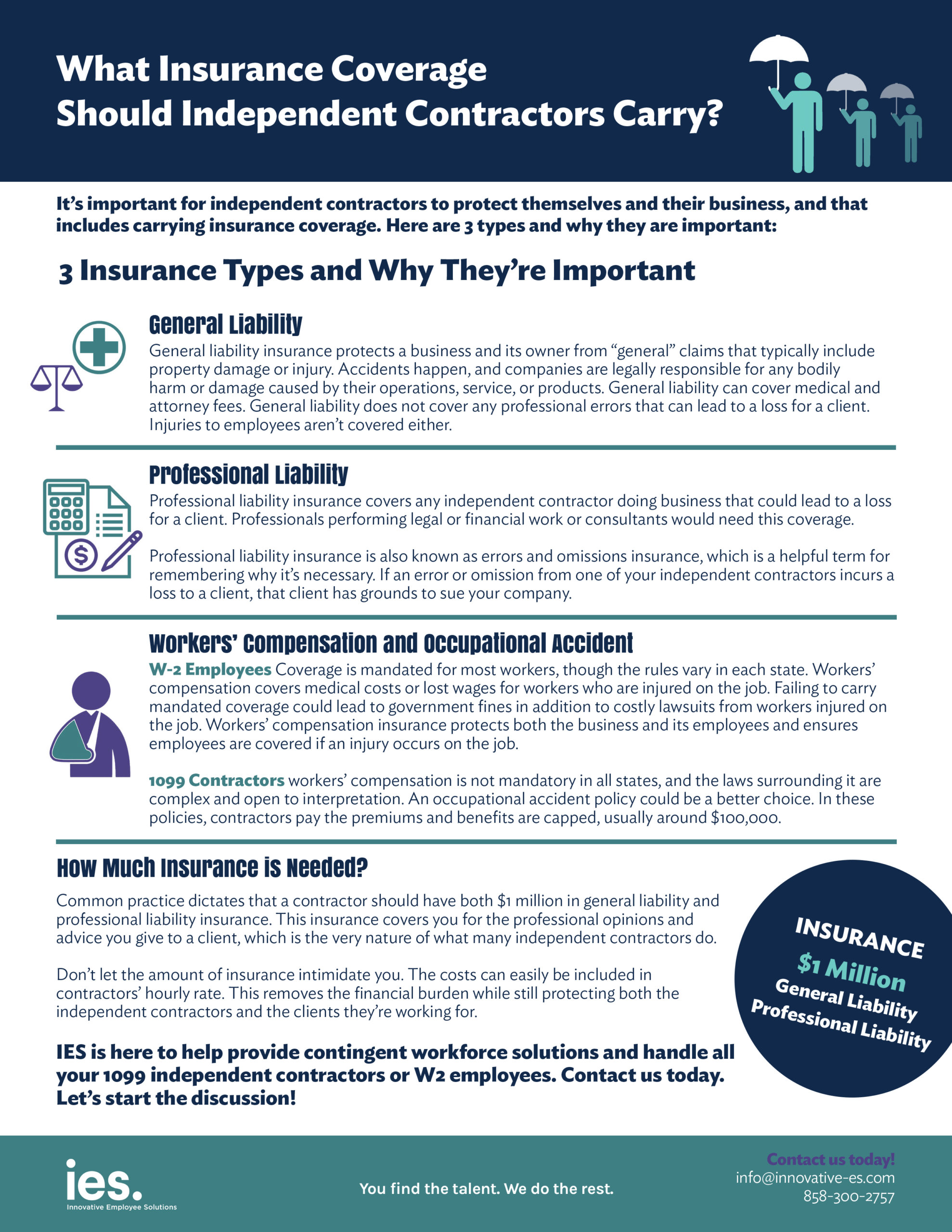

While general liability insurance is essential for most businesses, it may not always provide coverage for independent contractors. However, other insurance policies may extend coverage to independent contractors, depending on the nature of their work. These policies include:

- Professional liability insurance: This type of insurance, also known as errors and omissions insurance, provides coverage for claims arising from professional services. If your independent contractor offers professional services, such as consulting or legal advice, professional liability insurance may cover them.

- Workers’ compensation insurance: If your independent contractor gets injured while working for your business, workers’ compensation insurance may cover their medical expenses and lost wages. However, the eligibility for coverage can vary depending on local laws and regulations.

It’s important to carefully review the terms and conditions of your insurance policies to determine if they cover independent contractors. Additionally, consider consulting with an insurance professional to ensure you have the appropriate coverage for your business and its contractors.

Factors That Determine Coverage for Independent Contractors

When it comes to determining coverage for independent contractors, insurance companies typically consider several factors. These factors may include:

- Contractual agreements: If you have a written contract with your independent contractor that outlines the scope of their work and the terms of your agreement, it may affect their coverage under your insurance policy.

- Nature of work: The independent contractor’s work can also impact their coverage. Some insurance policies may have specific exclusions for certain high-risk activities or industries.

- Proof of insurance: Some insurance companies may require independent contractors to provide their coverage before extending coverage under your policy. This helps ensure that all parties involved have adequate protection.

It’s crucial to communicate openly and transparently with your insurance provider to understand the extent of coverage for independent contractors. This will help you avoid any potential gaps in coverage and protect your business from unexpected liabilities.

The Benefits of Extending Coverage to Independent Contractors

While extending coverage to independent contractors may not always be required or feasible, several benefits exist. These include:

- Improved risk management: Extending coverage to independent contractors can help mitigate the financial risks associated with their work. It provides additional protection for your business and covers any potential claims or lawsuits.

- Enhanced reputation: By offering insurance coverage to independent contractors, you demonstrate your commitment to their well-being and professionalism. This can help attract top talent and improve your reputation as a responsible and reliable business.

- Greater peace of mind: Knowing that your independent contractors are covered by insurance can give you peace of mind. It lets you focus on running your business without worrying about potential liabilities arising from your work.

Ultimately, deciding to extend coverage to independent contractors will depend on various factors, including your budget, the nature of your work, and risk tolerance. It’s essential to carefully weigh the benefits and potential drawbacks before deciding.

Conclusion

When it comes to whether business insurance covers independent contractors, there is no one-size-fits-all answer. It depends on your insurance policy, the nature of the work performed by the independent contractor, and the specific terms and conditions outlined in your policy. To ensure you have the appropriate coverage, review your policy, consult an insurance professional, and consider the benefits and drawbacks of extending coverage to independent contractors. By taking these steps, you can protect your business and make informed decisions that align with your needs and priorities.

Key Takeaways: Does My Business Insurance Cover Independent Contractors?

- Business insurance may not automatically cover independent contractors.

- Review your insurance policy to understand coverage for independent contractors.

- Consider obtaining additional coverage specifically for independent contractors.

- Consult with an insurance agent to ensure you have appropriate coverage.

- Regularly review and update your insurance policy as your business evolves.

Frequently Asked Questions

Here are some frequently asked questions about business insurance coverage for independent contractors.

Question 1: What is business insurance coverage for independent contractors?

Business insurance coverage for independent contractors is a type of insurance policy that protects them from the risks and liabilities associated with their work. It helps cover costs related to property damage, bodily injury, lawsuits, and other risks that may arise during their work.

While independent contractors are typically responsible for their insurance coverage, some businesses may require contractors to have their insurance policies to protect both parties involved in the business relationship.

Question 2: Does my business insurance policy cover independent contractors?

Whether your business insurance covers independent contractors depends on your policy’s specific terms and coverage. Some business insurance policies may include coverage for independent contractors, while others may not.

It’s important to review your insurance policy carefully and consult with your insurance provider to determine if your policy extends coverage to independent contractors. If not, you may need to explore additional insurance options to ensure adequate coverage for independent contractors working with your business.

Question 3: What are the potential risks of not having coverage for independent contractors?

Not having coverage for independent contractors can expose your business to various risks. If an independent contractor causes property damage or bodily injury while working for your business, you may be held financially responsible for the damages and legal expenses.

In addition, if a lawsuit is filed against your business due to the actions or negligence of an independent contractor, you may have to bear the cost of legal defense and potential settlements or judgments. Insurance coverage for independent contractors can help mitigate these risks and protect your business’s financial well-being.

Question 4: Can independent contractors purchase their insurance?

Yes, independent contractors can and often should purchase their insurance policies to protect themselves and their businesses. While some companies may require contractors to have their insurance coverage, even if it’s not mandatory, it’s wise for independent contractors to have their insurance policies in place.

Their insurance provides independent contractors with added protection and peace of mind, as they can tailor their coverage to their specific needs and ensure they are adequately protected from potential risks and liabilities.

Question 5: What type of insurance coverage should independent contractors consider?

The type of insurance coverage independent contractors should consider depends on the nature of their work and the risks involved. Some common types of insurance coverage for independent contractors include general liability insurance, professional liability insurance, and workers’ compensation insurance.

General liability insurance covers property damage and bodily injury claims. At the same time, professional liability insurance (also known as errors and omissions insurance) protects against claims of professional negligence or errors in the services provided. Workers’ compensation insurance provides coverage for work-related injuries and illnesses.

Independent contractors must assess the risks associated with their work and consult an insurance professional to determine the most appropriate coverage for their needs.

Final Summary: Does My Business Insurance Cover Independent Contractors?

After delving into whether business insurance covers independent contractors, it’s clear that there are a few key factors to consider. While every insurance policy is unique, business owners need to review their coverage thoroughly.

In conclusion, it’s important to remember that the extent of coverage for independent contractors can vary depending on the specifics of your business insurance policy. Some policies may provide limited coverage for independent contractors, while others require separate coverage. To ensure that you are adequately protected, it is recommended to consult with your insurance provider and discuss your specific needs regarding independent contractors. Doing so lets you make informed decisions and safeguard your business from risks and liabilities.

Remember, business insurance can be complex, but understanding your coverage is crucial. Take the time to review your policy, ask questions, and work closely with your insurance provider to ensure that you have the appropriate coverage for your business and any independent contractors you may engage with. By taking these steps, you can have peace of mind knowing that your business is protected and prepared for whatever comes its way.