If you’re wondering whether or not you have to pay taxes on life insurance, you’ve come to the right place. Taxes can be confusing, but don’t worry; I’m here to break it down. Life insurance is meant to provide financial protection to your loved ones in the event of your passing, but when it comes to taxes, you should know a few things.

Regarding the death benefit payout from a life insurance policy, the good news is that it’s generally tax-free. That means your beneficiaries won’t have to worry about paying taxes on the money they receive. However, there are some exceptions and specific situations where taxes may come into play. So, let’s dive deeper into life insurance and taxes to understand how it all works.

Life insurance proceeds are generally not subject to income tax. If you receive a death benefit from a life insurance policy, it is typically tax-free. However, there are some exceptions. For example, if you receive the death benefit in installments rather than a lump sum, the interest earned may be subject to income tax. Additionally, if the policyholder had previously transferred ownership of the policy, the proceeds may be subject to estate taxes. It’s always a good idea to consult a tax professional to understand your situation fully.

Do You Have to Pay Taxes on Life Insurance?

Life insurance provides financial protection for your loved ones during your death. It offers peace of mind and ensures your family will be financially cared for. But when it comes to taxes, many people wonder if they have to pay taxes on life insurance proceeds. In this article, we will explore the tax implications of life insurance and answer the question: do you have to pay taxes on life insurance?

Understanding the Taxability of Life Insurance Proceeds

Life insurance proceeds are generally not taxable, meaning your beneficiaries’ money from a life insurance policy is usually tax-free. This is because life insurance is considered a death benefit rather than income. Life insurance aims to support your loved ones financially, not generate revenue for the policyholder or the beneficiaries.

However, there are some exceptions to this general rule. In certain situations, life insurance proceeds may be subject to taxation. Let’s explore these exceptions in more detail.

Exceptions to Tax-Free Life Insurance Proceeds

While life insurance proceeds are typically tax-free, there are a few scenarios in which taxes may apply:

- If you have a cash-value life insurance policy and you surrender or cancel the policy, any cash value you receive may be subject to taxation. The cash value is the money accumulated in the policy over time.

- If you sell your life insurance policy to a third party in a life settlement transaction, the proceeds from the sale may be taxable. A life settlement involves selling your policy to a company or investor for a lump sum payment.

- Suppose you have a group term life insurance policy through your employer, and the coverage amount exceeds $50,000. In that case, the portion of the premium paid by your employer for coverage above $50,000 is considered taxable income.

- If you transfer your life insurance policy ownership to another individual or entity for valuable consideration, the transfer may be subject to taxation.

It’s essential to consult with a tax professional or financial advisor to understand your life insurance policy’s specific tax implications based on your circumstances.

Benefits of Tax-Free Life Insurance Proceeds

Life insurance proceeds are typically tax-free, providing several benefits to policyholders and their beneficiaries.

Firstly, it ensures that the policy’s death benefit goes directly to the intended recipients without tax deductions. This can provide much-needed financial support during a difficult time and help cover expenses such as funeral costs, outstanding debts, or ongoing living expenses.

Additionally, the tax-free nature of life insurance proceeds allows policyholders to maximize the money they can leave to their loved ones. By not having to account for taxes, individuals can choose a higher coverage amount to ensure their beneficiaries are well taken care of.

Planning for Taxes on Life Insurance Proceeds

While life insurance proceeds are typically tax-free, planning for the potential tax implications is still essential. By understanding the exceptions and seeking professional advice, you can make informed decisions about your life insurance policy.

If you have a cash value policy and are considering surrendering or canceling it, be aware of the potential tax consequences. Exploring other options, such as borrowing against the cash value or using it as collateral for a loan, may be beneficial to avoid triggering a tax liability.

If you are contemplating a life settlement, consult a financial advisor to assess the tax implications and determine if it’s the right choice for your financial situation. They can help you weigh the potential tax liability against the immediate economic benefit of selling your policy.

Transferring ownership of your policy should also be done with caution, as it can have tax implications. Consult with a professional to understand the potential tax consequences and explore alternative estate planning strategies.

Conclusion

While life insurance proceeds are generally not taxable, it’s essential to be aware of the exceptions and plan accordingly. Understanding the tax implications of your life insurance policy can help you make informed decisions and ensure that your loved ones receive the maximum benefit from your policy. Consult with a tax professional or financial advisor to navigate the complexities of taxation and explore strategies for optimizing your life insurance coverage.

Key Takeaways: Do You Have to Pay Taxes on Life Insurance?

- Life insurance benefits are generally not subject to income tax.

- If your life insurance policy earns interest, you may have to pay taxes on the interest portion.

- If you cash out your life insurance policy, you may have to pay taxes on any gains.

- Life insurance proceeds are usually not subject to estate tax.

- Consult with a tax professional to understand the specific tax implications of your life insurance policy.

Frequently Asked Questions

Question 1: Are life insurance payouts taxable?

Life insurance payouts are generally not taxable. The death benefit received by the beneficiary is usually income tax-free. This means the money received from a life insurance policy is not taxable federal income. However, a portion of the payout could be subject to taxes in certain situations.

For instance, if the policyholder had taken out loans against the cash value of a permanent life insurance policy and passed away before repaying them, the outstanding loan balance may be deducted from the death benefit. This could result in a smaller payout and potential tax liability on the remaining amount.

Question 2: Do I have to pay taxes on the cash value of a life insurance policy?

The cash value of a life insurance policy grows tax-deferred, meaning you won’t have to pay taxes on the cash value growth as long as the policy remains in force. However, if you surrender or cancel the policy and receive the cash value, any amount that exceeds the premiums you paid may be subject to taxes.

The loan is generally tax-free if you take out a loan against your policy’s cash value. However, if you surrender the policy or it lapses with an outstanding loan balance, the loan amount not repaid may be taxable as income.

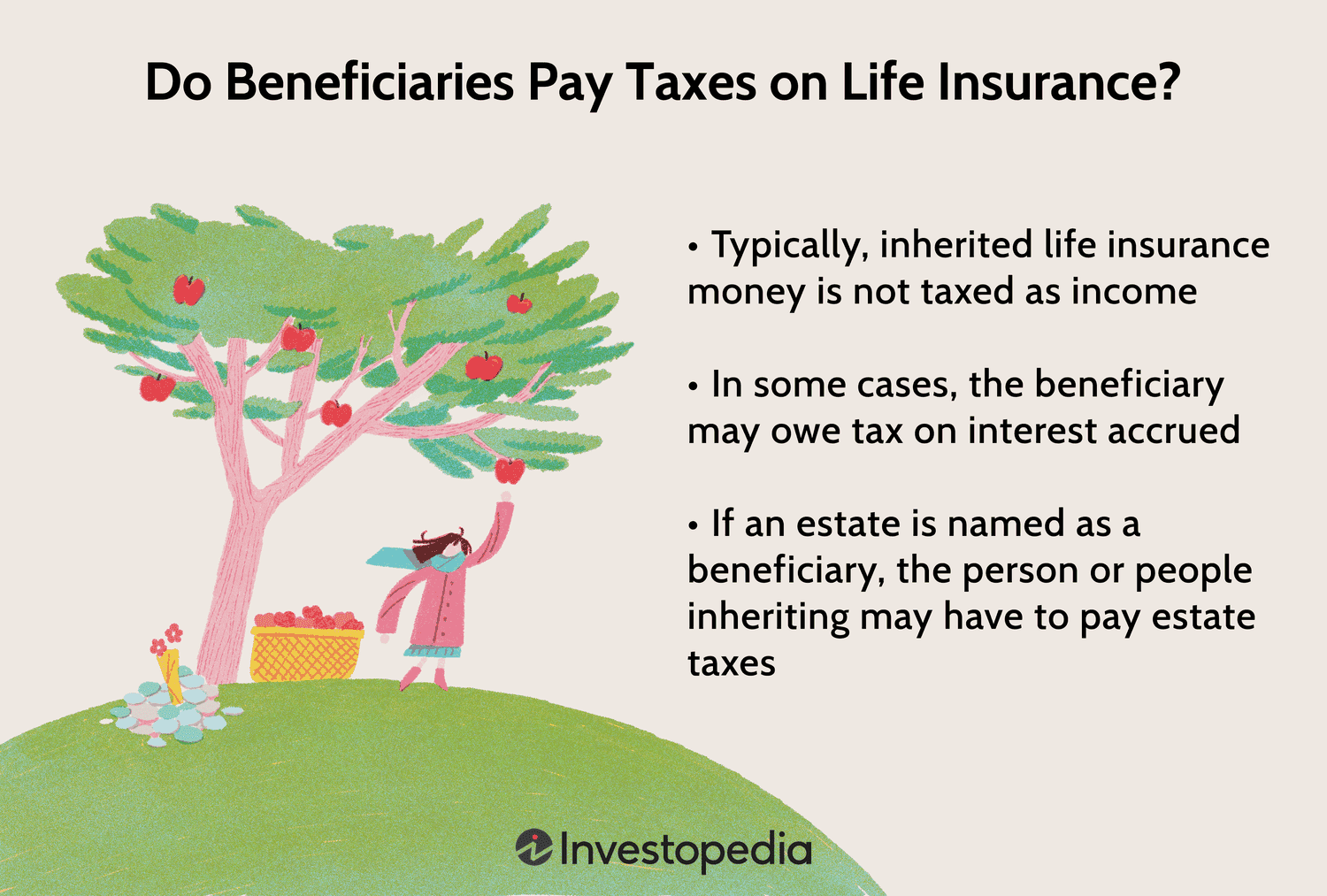

Question 3: Do beneficiaries pay taxes on life insurance proceeds?

In most cases, beneficiaries do not have to pay taxes on life insurance proceeds. The death benefit received from a life insurance policy is typically not considered taxable income. However, if the beneficiary receives the payout in installments and earns interest on the proceeds, that interest may be subject to income taxes.

It’s important to note that while federal taxes may not apply to life insurance proceeds, state inheritance or estate taxes could still come into play depending on the size of the estate and the state’s tax laws.

Question 4: Are life insurance premiums tax-deductible?

In general, life insurance premiums are not tax-deductible. The IRS considers life insurance a personal expense, not a business expense, so the premiums paid for a life insurance policy are not eligible for tax deductions.

However, there are some exceptions where life insurance premiums may be tax-deductible. For example, the premiums may be deductible if the life insurance policy is part of a qualified employee benefit plan, such as group life insurance provided by an employer. It’s best to consult with a tax professional or financial advisor to determine if you qualify for any deductions.

Question 5: Can I avoid taxes on life insurance by gifting the policy?

Transferring a life insurance policy to another person through gifting does not necessarily avoid taxes. Suppose you share a policy and retain any incidents of ownership, such as the ability to change beneficiaries or borrow against the cash value. In that case, the policy may still be considered part of your estate for tax purposes.

However, if you gift a policy and completely relinquish all ownership rights and control over the policy, it may be excluded from your taxable estate. It’s essential to consult with an estate planning attorney to ensure that any gifting strategy aligns with your specific financial situation and goals.

Final Summary: Do You Have to Pay Taxes on Life Insurance?

After exploring whether you must pay taxes on life insurance, it’s clear that the answer depends on various factors. While life insurance proceeds are generally not taxable, there are situations where taxes may apply. Understanding these nuances is essential to ensure you make informed decisions regarding your life insurance policy.

In most cases, the death benefit received from a life insurance policy is not subject to income tax. This means that if you are the beneficiary of a life insurance policy and receive a payout upon the insured person’s passing, you typically won’t have to worry about paying taxes on that amount. However, there are exceptions to this rule. For instance, if you receive the death benefit in installments, any interest earned on those payments may be subject to taxation. Additionally, the proceeds may be taxable if the policy was transferred for valuable consideration, such as being sold to another party.

Another important consideration is the cash value component of specific life insurance policies, such as whole life or universal life insurance. If you surrender the policy and receive a cash payout that exceeds the total premiums you paid, the excess may be subject to taxation. It’s crucial to consult with a tax professional or financial advisor to fully understand the tax implications of surrendering a life insurance policy.

In conclusion, while life insurance proceeds are generally not taxable, there are circumstances where taxes may apply. It’s essential to assess your situation, understand the tax laws, and seek professional advice to make the right decisions regarding your life insurance policy. By staying informed and proactive, you can navigate the complexities of taxation and ensure your loved ones receive the financial protection they deserve.